The stadtguthaben®-system enables cities to create, operate, and manage their own local payment infrastructure. It is a powerful tool to strengthen the local economy, foster community engagement and enhance the city’s overall attractiveness as a place to live, work and visit.

Why It Matters

Cities and regions face increasing pressure to remain economically vibrant and socially attractive. Large online platforms and global chains often draw money away from local economies.

A city-owned payment system reverses this trend by creating a closed, digital payment cycle that rewards local shopping, supports small businesses, and promotes regional identity. It’s a tangible instrument for city administrators and economic development agencies to boost local resilience, citizen loyalty and urban vitality.

Each city decides who can join the network, ensuring that local money circulates locally. This allows municipalities to strengthen local retail, restaurants, cafés and other service providers.

Smart Cities Keep The Money Local!

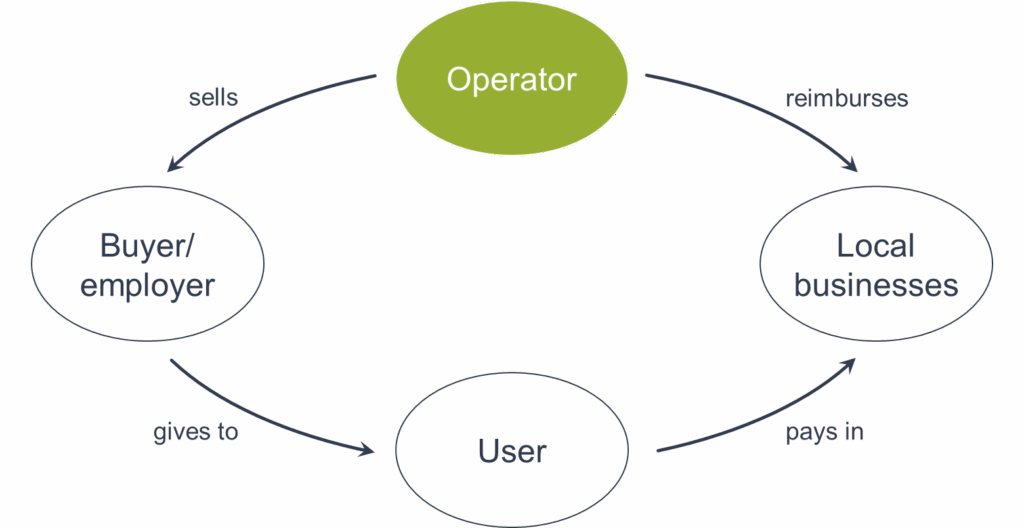

How It Works

The system is based on a simple and secure optical payment process using prepaid cards with QR codes:

- Operator/selling points can scan the QR code via our app or a web browser to load money onto the card. Vouchers (as PDF file) can also be bought online.

- Participating shops and restaurants scan the same card to redeem payments.

- The transaction amount is automatically deducted from the balance and added to the participant’s account. At this point, no money is transferred.

- The clearing process – the financial settlement between the city and the participant – is managed locally via SEPA-payment data generated by the system. All funds remain under the city’s control. This provides transparency, trust, security and flexibility for municipal administrators.

Regulatory Framework in Europe

Because digital payments are involved, regulatory compliance is an essential aspect. Within the European Union, the Payment Services Directive 2 (PSD2) defines the general framework for issuing and managing payment instruments.

However, PSD2 also includes specific exceptions under which such systems can operate without being subject to financial supervision.

This model falls under the Limited Network Exception, which applies when a payment instrument can only be used within a clearly defined network – such as participating local businesses within one city or region. This exception has been implemented into national law across EU member states, making the model legally viable and compliant throughout Europe. Regulatory details, however, may vary from country to country.